Q1 2026 Economic & Market Recap

Signal, Noise, and the Cost of Uncertainty.

The first quarter of 2026 reminded investors that markets rarely move in straight lines—especially when geopolitics, inflation, and monetary policy intersect. While economic fundamentals continued to point toward a slowing but resilient economy, markets once again spent much of the quarter reacting to uncertainty rather than outcomes. As we have stressed in previous commentaries, the key for long-term investors remains distinguishing between durable signal and temporary noise.

Economic Conditions: Slower Growth, Familiar Constraints

U.S. economic growth moderated during the first quarter as the cumulative effects of higher interest rates continued to work their way through the system. Consumer demand showed signs of fatigue in interest-sensitive categories such as housing and autos, while labor market conditions remained healthy but less tight than in prior years.

Inflation progress stalled somewhat as energy prices surged late in the quarter, complicating the decline in headline inflation measures. While core inflation continued to trend downward modestly, renewed pressure from commodities—particularly oil—served as a reminder that inflation risks have not yet been fully extinguished.

We wrote last December that the Federal Reserve was likely to stay on the sidelines through the remainder of Fed Chair Powell’s term ending in May. Markets were forecasting anywhere from 25 -75 basis points in rate reductions starting in June with the leadership transition to Kevin Warsh. That outlook has now shifted as the spike in oil prices puts renewed pressure on inflation. As of 3/31, markets were forecasting a better than 70% chance that rates would remain at current levels through the end of the year.

Energy Markets: Oil Surges on Iran Conflict

Energy prices became one of the most prominent sources of volatility during the quarter as the expanding conflict involving Iran disrupted global supply routes. Iran’s effective restriction of tanker traffic through the Strait of Hormuz—an essential chokepoint for global oil supplies—introduced a significant risk premium into crude markets.

Brent crude oil rose from roughly $62 per barrel at the start of the year to approximately $118 by March 31, while West Texas Intermediate (WTI) increased from roughly $62 to approximately $101 per barrel over the same period.

While prices moderated slightly toward quarter-end, the sharp increase in energy costs poses a stagflation risk, with upward pressure on prices and an expected drag on global growth.

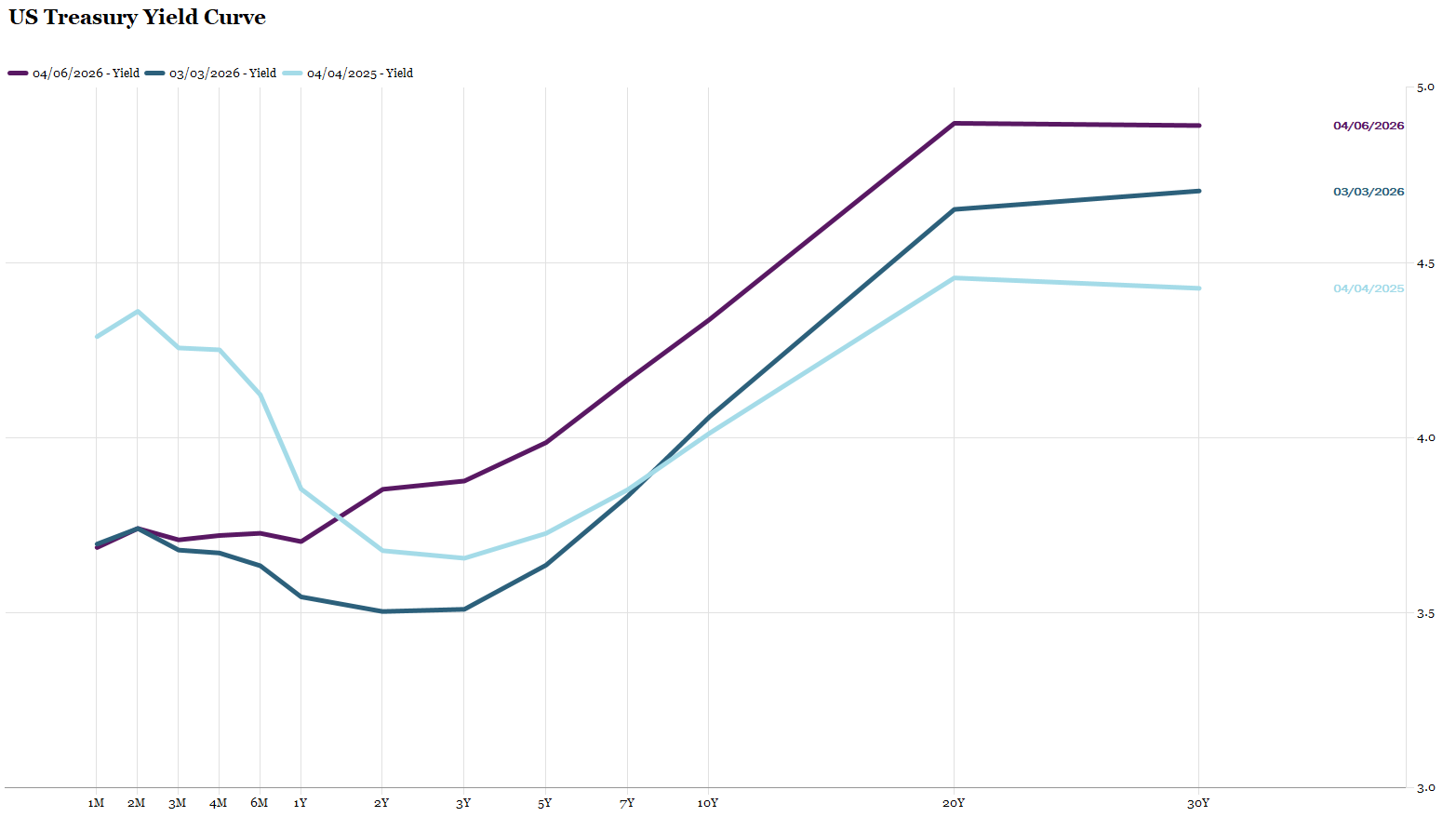

Fixed Income: Higher Yields Create Opportunity

Treasury yields moved higher during the first quarter as renewed inflation concerns reduced expectations for near-term policy easing. The 2-year Treasury yield increased from approximately 3.50% to 3.82%, while the 10-year Treasury yield rose modestly from roughly 4.26% to 4.30%.

Although higher yields weighed on bond prices in the short term, the reset in yields materially improves forward-looking return expectations. With a normalized, upward sloping curve we currently recommend a slight extension of duration within fixed income portfolios to take advantage of these elevated yield levels.

Equity Markets: Narrow Leadership, Global Divergence

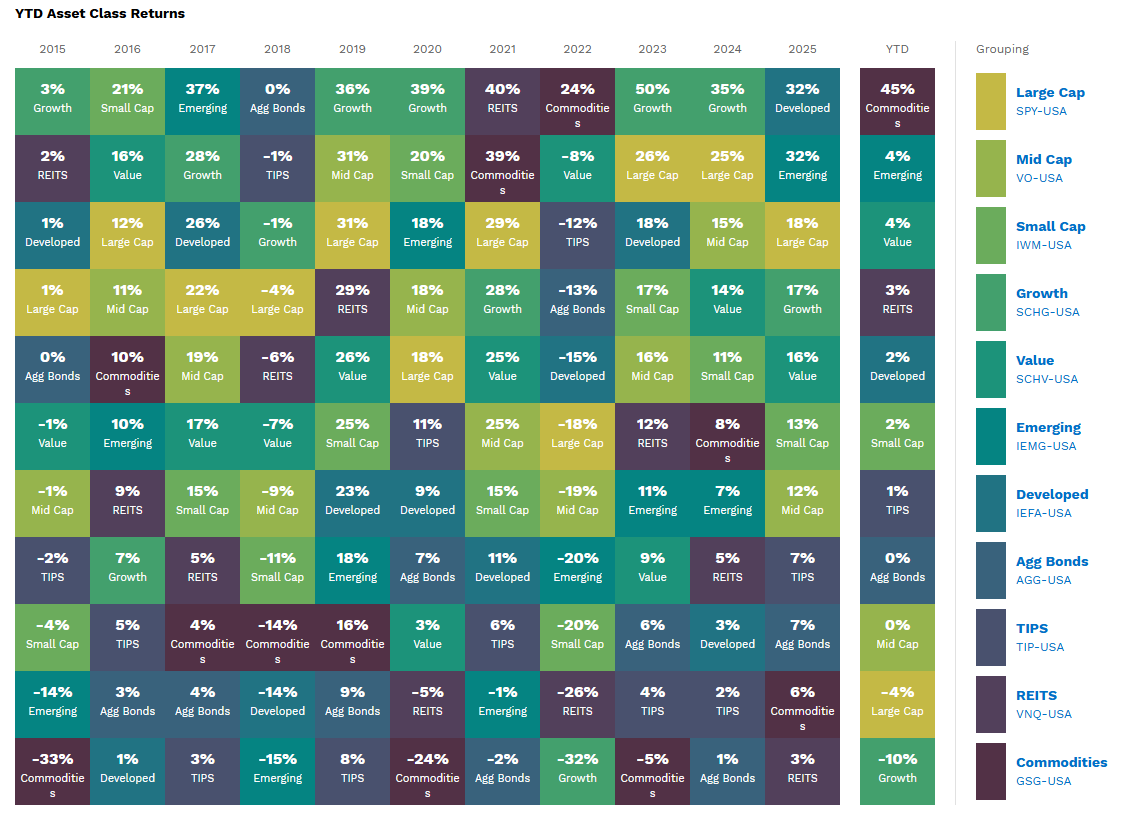

Equity markets delivered mixed results during the quarter. The S&P 500 Index declined approximately 4% year-to-date, weighed down by elevated valuations and concentrated leadership. Mega-cap growth stocks were hit the hardest this quarter, with the Russell 1000 Growth Index down over 10%. This marked the second quarter in a row where diversification provided portfolios with enhanced returns. Emerging markets and Large-cap Value led the way. Both categories have returned nearly 4% year-to-date. International Developed and Small-caps were also positive with each returning 2% for the first quarter. These divergences reinforce the importance of maintaining diversified, globally balanced portfolios.